Insulated From Reality

Europe's grid operators found a way to make 1,600 TWh of hydrogen volume appear on paper.

A perennial claim after energy shocks such as the one unleashed by Hormuz is that green hydrogen is the key to limiting Europe’s fossil fuel dependency. Exemplary of such ideas is this statement from the Hague Centre for Strategic Studies:

Transitioning away from fossil fuels is no longer just a climate strategy, it is a security strategy. Domestic renewable energy is, by definition, immune to geopolitical disruption. Wind blowing over the North Sea cannot be sanctioned. Electrolysers producing green hydrogen are not subject to Strait of Hormuz closures.

According to the EU’s REPowerEU plan, the bloc aims to massively ramp up its hydrogen production and imports. By 2050, renewable hydrogen is meant to cover around 10% of the EU’s energy needs. In 2022, all hydrogen—overwhelmingly produced from natural gas—covered less than 2%. Renewable hydrogen is supposed to displace gas in power generation and as a feedstock and heat source in industrial processes. As the Commission puts it: “Hydrogen stands as a key component in the EU’s strategy to the energy transition, net-zero, and sustainable development.”

However, neither domestic nor international green hydrogen production has seen an uptick to any meaningful extent that could cover Europe’s needs, despite member states having spent about €20 billion in subsidies in recent years. Normally, you’d assume that when a technology repeatedly fails to deliver, common sense eventually dictates that funding stops.

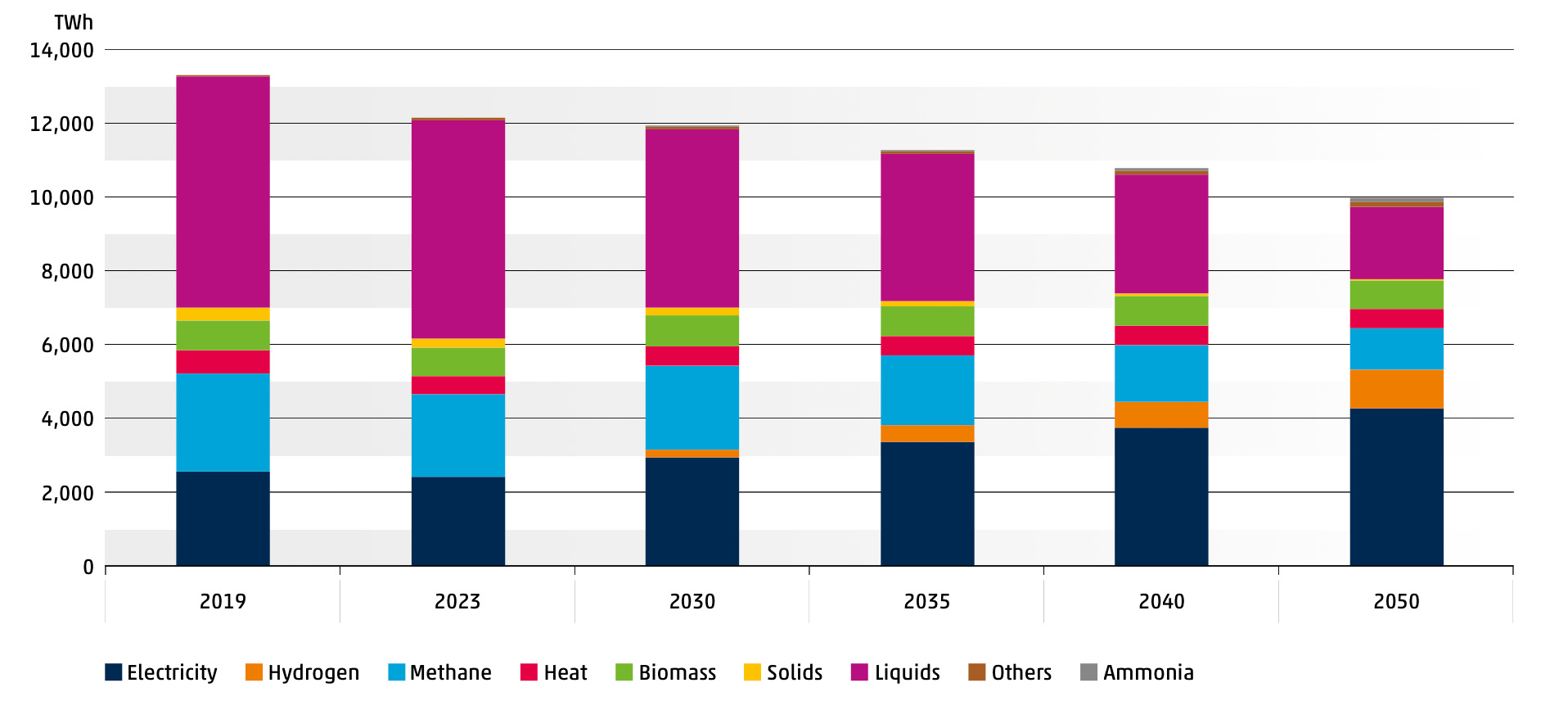

But last week’s Draft Scenarios for the Ten-Year Network Development Plans (TYNDP) by ENTSO-E and ENTSOG—the European associations representing national electricity and gas transmission operators—confirm not just the unwavering political commitment to the hydrogen goal. According to this paper, hydrogen should displace gas by 1,600 TWh/year by 2050.

Reaching even half that target through domestic electrolysis is functionally impossible. Generously assuming 80% electrolyzer efficiency, it would require roughly 1,000 TWh of electricity: almost exactly as much as all of Europe’s wind and solar generation combined in 2024, using Statistical Review of World Energy figures.

It took about 25 years to build Europe’s current wind and solar fleet. Replicating that entire buildout once more in the years remaining, and dedicating every bit of the new capacity solely to hydrogen, is exactly as visionary as the Net Zero Industrial Complex™ likes to present itself.

While some of that volume may eventually be covered by nuclear-powered hydrogen production, the bulk would have to be bought on a market that can’t deliver such volumes. Time to check what it takes to make them appear on paper.

In a normal market, when two products do roughly the same job, customers buy the cheaper one. That's the simplest explanation for why hydrogen remains a niche industrial input rather than an energy-transition cornerstone. Most of what the report counts toward that 1,600 TWh is this kind of interchangeable use—gas turbines, boilers, and trucks that can in principle switch fuels—yet the price difference between gas and green hydrogen borders on the absurd.

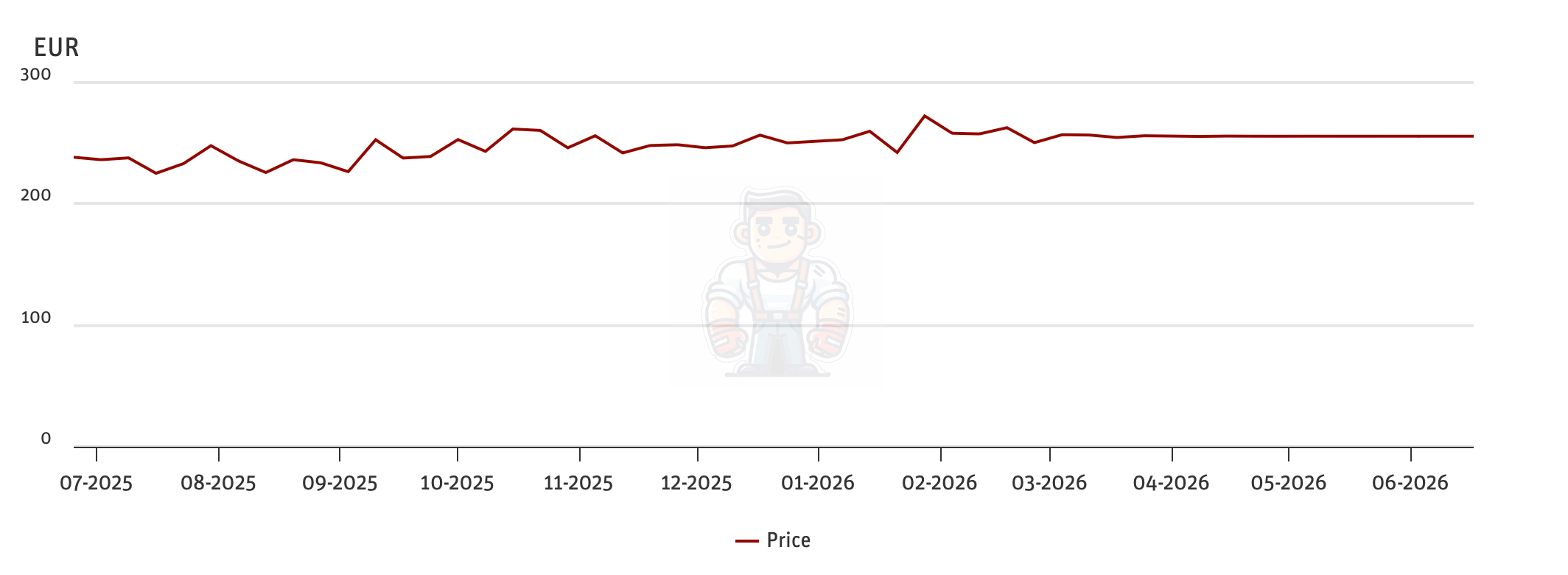

HYDRIX, the EEX’s weekly market-price benchmark for green hydrogen delivered to German consumers, currently puts that price at €256/MWh. Far from falling as the market matures, it has risen from €238/MWh in the earliest data EEX’s tool shows (June 2025), holding flat near current levels since roughly March 2026.

Cost estimates from the Institute of Energy Economics at the University of Cologne assume the opposite trajectory: domestic German production at roughly €240/MWh today, falling to €200/MWh by 2030, with pipeline imports from North Africa cheaper at €150-170/MWh. Shipped ammonia imports run €250-300/MWh due to conversion and transport losses.

LNG, meanwhile, has traded on the Dutch TTF benchmark between roughly €30 and €50/MWh over the past year. Even hydrogen's cheapest pathway costs three to four times more than gas.

Given this insurmountable price difference, none of the gas substitution happens through ordinary supply and demand. So how does the ENTSO-E report get from that gap to 1,600 TWh of hydrogen anyway?

ENTSO-E's methodology answers that question. Half of all import capacity gets secured through long-term contracts—the kind of take-or-pay structure used in LNG deals, where a buyer commits to a fixed volume regardless of price. The report does not state what these contracts actually cost or how the price will be determined. Instead, the model ranks supply sources cheapest-first to decide what gets used. Then it assigns these contracted volumes a modelled cost of zero, guaranteeing they're used before anything else.

The not-so-unwelcome side effect is that this system is insulated from price signals because the contracts pay out the same whether the bet on hydrogen turns out right or wrong. The cost to tax- and ratepayers will likely be folded into grid fees and EU budget allocations spread across dozens of programs that obscure the true cost of the shift.

In any other market, a bad bet surfaces and gets corrected: prices adjust and capital moves elsewhere. But there's no “elsewhere” in hydrogen—every pathway is expensive, which is why only contracts immune to price make building capacity rational in the first place. No producer sinks capital into electrolysers and export terminals otherwise, because everything else about this trade argues against it.

Infrastructure is the clearest example: what gas has that hydrogen doesn’t is decades of pipelines, storage caverns, and power plants built and paid for. Hydrogen's equivalent network barely exists, because the underlying resource gives producers no reason to build it.

Despite occasional crisis-driven shortages, which are more distribution than production problems, the world has all the natural gas it needs: as of 2021, there were an estimated 7,299 trillion cubic feet (Tcf) of total world proved reserves compared to annual consumption below 145 Tcf in recent years. Given this abundance, there is no economic incentive to even attempt a hydrogen switch on any timeline that matters.

China will inevitably come up as the counterargument: no country pushes harder on hydrogen. Yet even there, hydrogen is just one mosaic piece in an energy-security portfolio that runs heavily on coal. On an energy-equivalent basis, China’s coal-to-liquids (CTL) capacity—11 million tonnes of synthetic fuel in 2023—outweighs its green hydrogen sector—220,000 tonnes per year—roughly 16 times over.

China’s build-outs reveal what the country actually bets on with capital. Europe’s auditors have reached the same conclusion on paper. As Germany’s Federal Court of Auditors put it in late 2025:

Expectations that green hydrogen would become price-competitive have not been fulfilled so far. Rather, hydrogen will remain expensive going forward as well. Permanent government subsidies are therefore foreseeable as a result.

The EU’s Court of Auditors said much the same a year earlier, in 2024, finding the Commission’s hydrogen targets unrealistic and “driven by political will rather than being based on robust analyses.” Two independent institutions, the same verdict, and the subsidies keep flowing anyway.

Ursula von der Leyen stressed the role of hydrogen once again at the recent EU–South Korea summit in Brussels, shortly before the grid operators’ report went public. Committing increasingly scarce capital to a bet insulated from ever being proven wrong is a vulnerability in itself. The biggest risk to Europe’s energy security may not sit at the Strait of Hormuz but 5,000km away.

Share this article with anyone watching the wrong chokepoint!

📨 People in boardrooms, energy desks, and hedge funds keep forwarding this. Stop getting it late — subscribe now!

The biggest threat to Europe has always been in Brussels.

since H2 (and don't bother to use the word "green" that's a fantasy) is not available in it's "free" IE not bound up in a molicule, state, Hydrogen is nothing but a very fancy and rather expensive battery. You have to put a shit ton of energy in to crack the hydrogen out of your feedstock. It doesn't matter if the feedstock is amonia, water, natural gas... You have to put in energy to get it out.

The three primary rules of physics cannot be broken. You don't get out as much as you put in. There is no such thing as a free lunch, or a 100% conversion. So, you loose energy in the process of getting the H2. Further as a battery it has some very dificult (IE expensive) problems, including Hydrogen embrittlement, and, oh, the Hindenburg factor.

At some future date, it MAY be the most practical way to transfer energy from the electrical grid to an automobile, but that day is not here yet. To sell it as the cure to a nation's energy crisis only works if the people you're selling it to are scientifically Illiterate.