Pricing the Invisible

The war broke oil price discovery. The peace deal won't fix it.

Coming to terms with the price of oil is a boon for everyone creating content in the financial space right now. The fact that a disruption at the most important chokepoint in the world's fossil fuel supply causes both WTI and Brent to hover around $100 lets people come up with all kinds of explanations ranging from sober to wild: from it being merely a logistics crisis in a market that has proven far more resilient than almost anyone expected, to elaborate explanations claiming suppressed oil futures prices are part of a US grand strategy designed to drain China's dollar reserves and collapse the offshore yuan.

While crazier conspiracy theories have turned out to be correct, the idea that no one will take the other side of a suppression trade would be quite the outlier in the world of commodity trading. Vitol, Trafigura, and Glencore would be printing free money: buy cheap paper, take physical delivery, sell into the real market. With an arbitrage opportunity this enormous, the gap would close.

The deeper problem with the claim that $100 oil is not the "correct" price is that this thinking is backwards: those commenters are so certain about the eventual outcome—massive physical shortage, prices far higher—that they work from that end result and conclude any current price that does not reflect it must be fraudulent. The certainty about the future state is being used to invalidate the current market price. Occam’s razor tells us the simplest explanation tends to be correct, and Doomberg put it plainly back in April:

Effectively, the markets are pricing a binary outcome: a long war and the potential for catastrophic damage to priceless assets, or a sudden peace and the rush of supply it would bring. If one scenario implies $150 oil and the other $50, is a rough price of $90 all that far off?

However, it is one thing to ask which price is right today. The more persistent question is whether anyone pricing physical supply has ground truth to work from. As Oil & Gas 360° wrote this week:

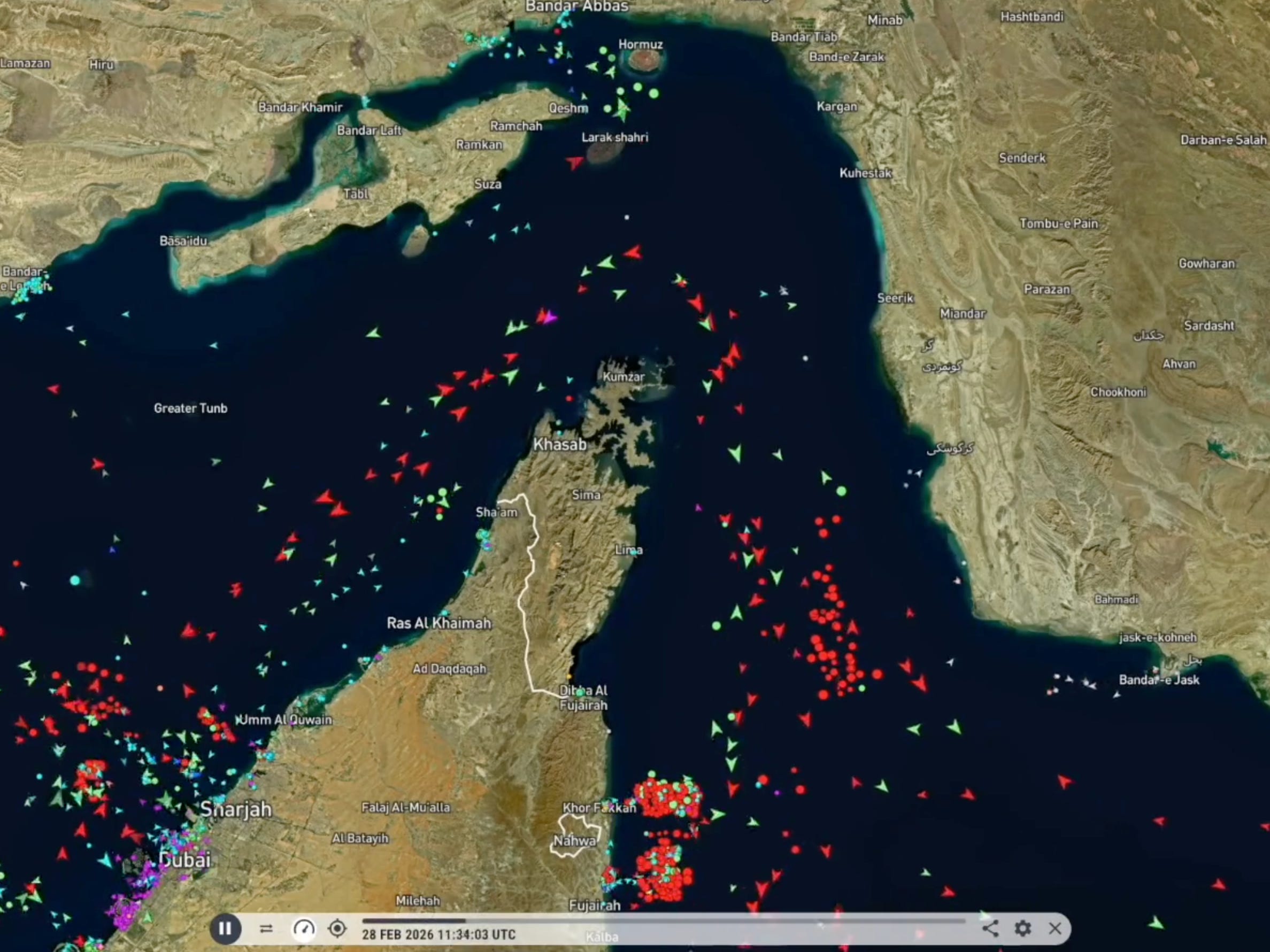

More vessels are leaving the region after passing the Strait of Hormuz in a dark mode with transponders switched off, and those entering the Persian Gulf to load cargoes are increasingly doing the same.

The dark-mode tactics, once the feature of Iran-linked vessels aiming to skirt sanctions, are now the norm for the majority of commercial traffic at the Strait of Hormuz.

The threat to tankers attempting to pass the Strait of Hormuz has created a new shipping reality. Dark-mode activity, with transponders switched off, is no longer for Iran-linked vessels only. It has spread to commercial shipping of non-sanctioned barrels and other goods that typically move through the chokepoint, data from Vortexa showed last week. Dark transits through the Strait of Hormuz have accounted for 57% of all transits recorded over the period, peaking at 65.2% in May.

A visibility floor as low as 35% at its May peak raises the question of who knows what is moving and who does not. Regardless of whether this conflict ends in the peace deal currently on the table or remains latent for years, that question is permanently reshaping price discovery in oil markets. Time to take a closer look.

Under the International Convention for the Safety of Life at Sea, every cargo vessel above 300 gross tons on an international voyage is required to broadcast continuously on the Automatic Identification System (AIS). This is a VHF radio protocol that transmits position, heading, speed, destination and draught: the vessel’s depth in the water, which acts as a real-time proxy for how much it is carrying. Since that figure is self-reported, it is frequently unreliable. The system was originally designed for collision avoidance but became, in the absence of anything better, the primary data source for global oil market intelligence: the feed behind flow estimates.

One partial substitute for AIS is synthetic aperture radar (SAR) via satellite. SAR confirms a hull is present at the time of the orbital pass, but none of the details AIS would provide. What it can establish is how many vessels are operating without AIS. The gap from pre-conflict norms is substantial. Windward—a maritime intelligence firm whose satellite collections include radar and optical imagery alongside AIS analytics—surveyed the broader Hormuz area on 5 May and identified 167 commercial vessels, 146 were operating dark. A separate SAR collection the following day focused on the northern corridor: 97 vessels, three were transmitting AIS.

Since oil price discovery is such a big business, analysts use all the mosaics they can get in the absence of more reliable data. One method to track oil flows is satellite imagery of oil storage. Large tanks are fitted with floating metal roofs that ride on the liquid surface, rising as tanks fill and falling as oil is drawn. The shadow the roof casts against the inner tank wall reveals fill levels. Tracking those readings at Gulf origin terminals and destination storage facilities allows analysts to recover some of what dark transits remove.

But that method is only an imperfect substitute. Matt Smith, Kpler’s Director of Research, noted in a recent interview that the product inventory draws that would confirm dark cargoes arriving in Asian terminals are “in opaque areas and we just cannot see that right now.” More fundamentally, the Gulf storage cross-check tells you what happened in the past while transit data is a real-time signal. Oil price formation runs on the real-time clock, and a backward-looking confidence check is of limited help.

Not everyone is flying blind, though. In March 2026, Iran began requiring vessels to seek permission before transiting the Strait. In May it formalised the arrangement: the Persian Gulf Strait Authority (PGSA), administered by the IRGC Navy, went live with a domain name, an official email address, and a transit-permit regime.

Before a vessel receives authorisation, it must submit what the PGSA calls a Vessel Information Declaration: over 40 questions covering ownership, insurance provisions, crew manifests, cargo details, past port calls, and intended routing. A permit is issued only after the PGSA accepts the submission and a fee of up to $2 million, paid in yuan or Bitcoin, is settled.

The PGSA’s cargo manifests give Iran comprehensive intelligence on flows before vessels move. In price formation, who knows first prices first. The logic is that of payment for order flow: see the order before the market does, price accordingly. With the Strait of Hormuz representing 20-25% of global maritime oil trade, Iran will want to keep a system in place that preserves that informational advantage even if it dispenses with the toll fee. And as the US is increasingly insulated from Middle Eastern supply, the PGSA’s informational architecture may not even register as a concession worth demanding.

Foreign Minister Abbas Araqchi has already insisted that the administration of the Strait of Hormuz “will not return to the pre-war era.” Such arrangements tend to have remarkable durability. As Jess Hoversen points out, Denmark controlled the Øresund Strait from 1429 to 1857. Even after Denmark lost the eastern shore to Sweden in 1658, the toll system stayed in place for another 199 years.

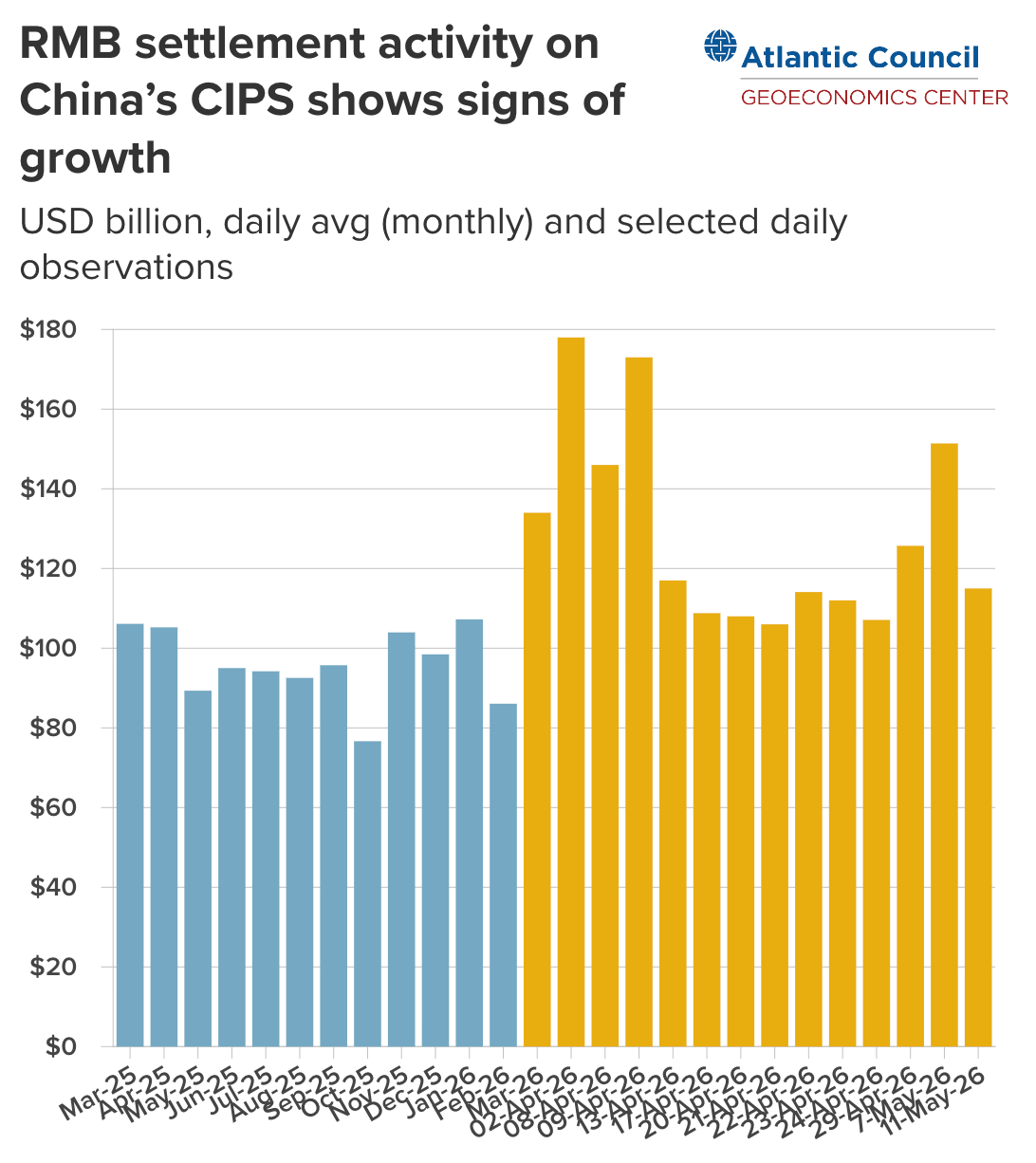

The payment infrastructure for non-dollar energy settlement is scaling rapidly alongside the conflict. CIPS, China’s dollar-alternative interbank settlement network, processed an average of $134 billion per day in March 2026, a 50% surge from February that coincided exactly with the conflict’s onset. While this is not direct proof of PGSA-linked flows, it indicates that capital will find ways to monetise an informational advantage of this scale, inside or outside Western settlement systems.

The “correct” price of oil will remain elusive. Dated Brent and Dubai assessments are constructed from visible, Western-compliant transactions. PGSA-corridor flows—yuan-settled, excluded from assessment windows—contribute nothing to those assessments. What the benchmarks record is increasingly the price of what stays visible: a shrinking fraction of the market, self-selected for Western compliance. Traders pricing oil from those benchmarks are working from a signal with a growing blind spot.

Share this article with anyone who thinks the Strait reopening is the end of it!

📨 People in boardrooms, energy desks, and hedge funds keep forwarding this. Stop getting it late — subscribe now!

40+ years in markets informs me that the 'right' price for oil is the price on the screen. market signals simply cannot be ignored. it can be no surprise that the recent stories of 7mm bpd more than expected have been flowing out of the Strait given the fact that oil's price simply has shown no inclination to rise dramatically. your point about Vitol et al profiting hugely from any dislocation is exactly correct, and in so doing they help drive the known price.

I think the other thing that is happening is not only is the US producing more, but so is Canada, Guyana, Venezuela, Brazil and even Argentina. at $90/bbl or $80/bbl, drillers gonna drill.

Ships carrying Iranian oil are likely to go 'dark' to evade the US semi-blockade. Its very difficult to be sure of origin.

There is a lot made of the apparent fall in Chinese imports, which some are tying to draw down of their ample reserves and others to economic output reduction. I have seen no reliable evidence of either. I doubt anyone in the West has a real handle on Chinese imports and what it is getting from Russia.

The 'green bird' is a strong advocate of US exceptionalism along with one or two other analysts on substack. Currently I take their conclusions that the Hormuz situation is a nothing burger with a packet of salt. And as I have commented elsewhere, it may apply to the US but not to Europe or Asia.