Committed to Nothing

On the chances of a Gulf-European pipeline

When Iranian missiles hit Ras Laffan in Qatar on March 18, 2026, someone in Turkey must have popped the champagne. With the Strait of Hormuz effectively closed since late February, Qatar’s export capacity already sat bottled up inside the Gulf, unable to reach its customers. The strike on the world’s largest LNG export facility with a capacity of about 77 million tonnes per year (mtpa) turned a temporary disruption into a multi-year problem.

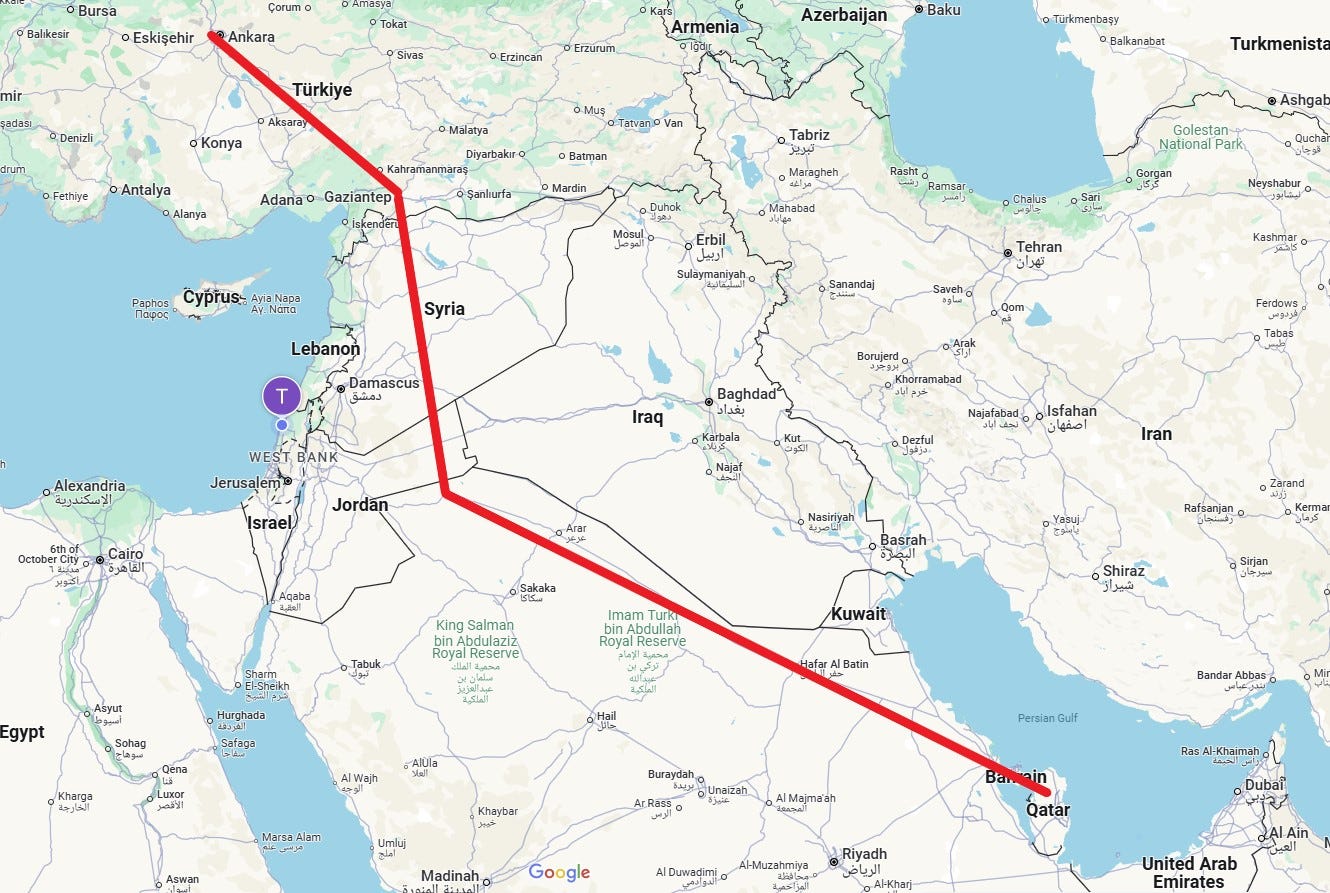

That situation likely reignited one of Ankara’s most persistent infrastructure ambitions: a pipeline from Qatar’s North Field to Turkey. A 1,500-kilometre (930 miles) route that would connect Gulf gas reserves to European markets for the first time without a single tanker. For Turkey, which has long sought to become Europe’s primary energy hub, it would represent a generational opportunity.

Turkish and Qatari leaders publicly endorsed the idea back in 2009, but the project was blocked by Syria’s Bashar al-Assad. This was reportedly due to Russian pressure. When Assad fell in December 2024, Turkey moved to revive it. Qatar’s foreign ministry called the idea “media speculation” in January 2025.

Then came March 2026. Qatar has now lost 17% of its export capacity and an estimated $20 billion in annual revenue. Its main export route has been mined and may remain problematic long after the conflict subsides. A pipeline to Turkey would circumvent the world’s most critical energy chokepoint. The logic seems compelling. And yet Qatar remains silent.

The project would require sustained alignment among multiple countries from start to endpoint: Qatar, Saudi Arabia, Jordan, Syria, and Turkey. That’s a high bar, but just one problem. The more fundamental obstacle to Turkey’s energy hub ambitions becomes visible on the other side of the Atlantic. Let’s hop to Texas for the bigger picture.

Twelve days after the Ras Laffan attack, another piece of QatarEnergy news got drowned in the noise. On March 30, Golden Pass achieved first production of LNG at its Sabine Pass terminal in Texas. The facility started life in 2010 as an LNG import terminal, built to bring gas into the United States. QatarEnergy and ExxonMobil took the final investment decision to convert it into an export facility in February 2019, committing more than $10 billion to the project. QatarEnergy holds 70%, ExxonMobil 30%.

The feed gas comes from American shale, primarily the Haynesville and Permian basins. Notably, Golden Pass, once at full capacity, will produce 18.1 million tonnes per year (mtpa), significantly exceeding the 12.8 mtpa knocked offline at Ras Laffan. With the Sabine Pass sitting on the Gulf of Mexico, this project also has the obvious advantage of being outside a war zone.

Golden Pass is the most prominent piece of a portfolio that QatarEnergy has been assembling for over a decade across four continents. The company holds exploration and production stakes in more than twenty countries—Namibia, Guyana, Brazil, Egypt, Mozambique among them—almost all of them outside the Persian Gulf. The logic running through every acquisition is to hold production equity beyond the reach of any single chokepoint.

Geographic diversification is only half the architecture. The other half is the structure of customer relationships. Here too Qatar has built in layers of protection for itself that its buyers do not share. When supply is disrupted, not all customers are treated equally.

QatarEnergy declared force majeure on contracts with Italy, Belgium, South Korea, and China, meaning delivery obligations are suspended and damage claims barred. Of the European buyers, Italy and Belgium face the greatest pressure due to their heavier reliance on Qatari supplies. According to Kpler, Qatar accounted for around 30% of Italy’s LNG imports and 8% of Belgium’s last year. Italy’s Edison will have to forgo 10 contracted cargoes mid-June alone.

The lost revenue from the Ras Laffan disruption makes a pipeline to supply these customers look attractive. But it would also be a permanent surrender of what QatarEnergy’s strategy is designed to preserve: non-commitment.

Commitment is the concept Qatar’s customers seem to have not properly taken into account. An LNG long-term contract binds the buyer. It binds the seller to a lesser extent. The decisive question is commitment depth: how physically bound is the supplier to deliver. An LNG long-term contract contains force majeure escape clauses created for the conditions when supply matters most: war, infrastructure damage, Hormuz closure.

A pipeline is different in kind. It requires billions in upfront capital that only pays back over decades of throughput at a negotiated price. That investment is a costly, physical signal that the seller has tied its return to one buyer, one route, and one price.

The obvious objection to the pipeline as a deeper commitment argument is Russia. In 2022, it demanded ruble payments, then cited a missing turbine, then suspended supply indefinitely in September 2022. Officially for technical reasons which the EU disputed, and four months after the EU had announced its intention to end Russian gas dependency.

Whichever version is correct, the physical result is the same: Gazprom posted a net loss of $6.9 billion in 2023—its first since 1999—because the Yamal fields that supplied Europe are not connected to China and have nowhere else to go. More than twenty trillion cubic meters of reserves, staying in the ground.

While pipeline dependency makes you vulnerable to a supplier's political will, LNG dependency makes you vulnerable to a supplier's commercial logic. Neither approach is safe. But a pipeline embodies deeper reliance than any LNG contract can match. It’s worth noting that Russia has repeatedly signaled that it stands ready to resume long-term cooperation with European customers if they are willing. A pipeline from an “enemy” is more committed than LNG from a “friend.”

Given Europe’s insistence on never returning to Russian gas, Turkey might hope that the EU will lobby for its pipeline project. After all, the EU’s only relevant pipeline supply comes from one country: Norway. The pipeline share of total gas imports fell from 77% in 2021 to 52% today.

Yet Qatar’s strategy demands it keep saying no to the project. Its commercial model depends on preserving optionality. Golden Pass is the tell: additional LNG capacity, different ocean, no long-term customers. QatarEnergy invested $10 billion to build 18.1 mtpa of new capacity and left the Golden Pass volumes uncontracted. A pipeline customer is the opposite: permanently tied to one route. Qatar would be cannibalizing its own LNG revenue while permanently surrendering a tranche of production to one buyer. Every molecule in the pipe is a molecule withdrawn from the global arbitrage.

Watch Europe’s post-Hormuz policy response. The right lesson would redirect capital toward constraint-side infrastructure: pipelines, storage, nuclear restarts. These are the only solutions that hold when force majeure arrives. Increasing the reliance on suppliers whose business model depends on flexibility is the absence of a security strategy. If Europe’s primary response is more LNG contracts, it will have repeated the same mistake with different suppliers: the commitment depth denominator ignored again.

Share this with anyone who thinks LNG is a security strategy!

📨 People in boardrooms, energy desks, and hedge funds keep forwarding this. Stop getting it late — subscribe now!

Already subscribed? Thanks for helping make BSJ quietly viral.

Beautiful insight. A bigger potential (probable) problem is the Turks themselves: they have perfected blackmail and hoatage-diplomacy. Erdogan declares "Asad must go", infiltrates Islamists into Syria, destabilises and loots the country, then cries like a spoilt child for help with refugees...and when he doesn't get what he wants, he weaponises the refugees and "Opens the Gates of Europe". This carpet-trader mentality is not unique to him: when China wanted to by a a half build aircraft carrier from Ukraine, Erdogan's predisessors blocked it and made a deal (citing the Montreux Convention) and relented after ballistic missile technology transfer was granted. Is Europe really going to give Turkey leverage with life and death resources control? A Turkey that has openly stated the desire to obtain nuclear weapons.

I’m still amazed that any sensible (the operative word here) European leader could look at that map, see that most of it’s energy options rely on stability in historically unstable regions, and yet continue to double down on proven destructive energy policies. This is ideology devolving into mental illness. And yet, I’ll repeat the truth I have learned, with very few exceptions, most people around the world have the government they deserve.